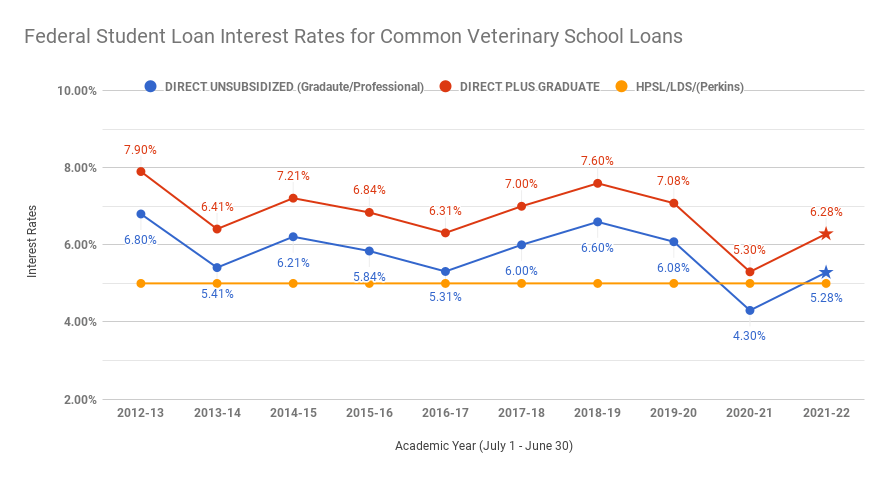

Each spring, we closely monitor the U.S. 10-year Treasury yield to see the final number setting the federal student loan interest rates. For the 2021-22 veterinary school academic, the answer is higher interest rates than last year, but some of the lowest interest rates seen in the last decade.

Federal student loan interest rates are updated each year using the high yield of the May U.S. 10-year treasury note. The high yield plus a factor for your Direct loan and school type sets the fixed rate you pay for the life of those loans received between this July 1st and next June 30th. As a veterinary student, the graduate/professional school Direct Unsubsidized loan interest rate will be 5.284%, up from 4.3% last year. The Direct Graduate Plus loan rate will be 6.284%, up from 5.3% last year.

Fortunately, the pandemic forbearance period that started on March 13, 2020, set interest rates to 0% for eligible federal student loans. This special forbearance will continue through at least September 30, 2021. Therefore, all your eligible federal student loans, even those loans you receive for the start of the 2021-22 academic year, will be interest-free for a bit longer. The impact of the pandemic forbearance for veterinary students has been quite beneficial, significantly lowering the interest that you normally accrue during veterinary school.

The importance of your school Cost of Attendance

Do not borrow more than you need because student loan interest rates are zero for a little while longer. The less you borrow, the less interest accrues (long-term) and the less you’ll have to manage in repayment. Always review your school’s published cost of attendance (COA) and look for ways to reduce the loans you accept in your financial aid awards.

As a graduate/professional student, you’re frequently offered student loans to cover the full COA. Use your budget to determine if you actually need to take all the loans you are offered. The COA is the maximum amount you can borrow. Your mission, if you choose to accept it, will be to accept less in loans than the maximum COA.

Reducing loan awards and returning loans vs. paying interest during school

Too many veterinary students are paying interest on their student loans while they are in school. If you are paying interest on your student loans as a student, ask yourself where that payment money comes from. If you’re using federal Direct student loans to pay down other federal Direct student loans, you’re not gaining any ground. Even if the funds you’re using are coming from your veterinary school job or from the help of a significant other, a less expensive plan would be to borrow less rather than paying interest. Reduce your future loan awards or return loans that you received above your budgeted need to make the biggest impact on your total debt balance. You have up to 120 days to return the loan amounts you received that you might not need. When you return student loans, the principal, interest, and fees are also returned. Therefore, the loans you don’t borrow or the principal you return within the 120-day window goes much farther than paying the interest alone. To learn more, visit the VIN Foundation Borrow Better resource page.

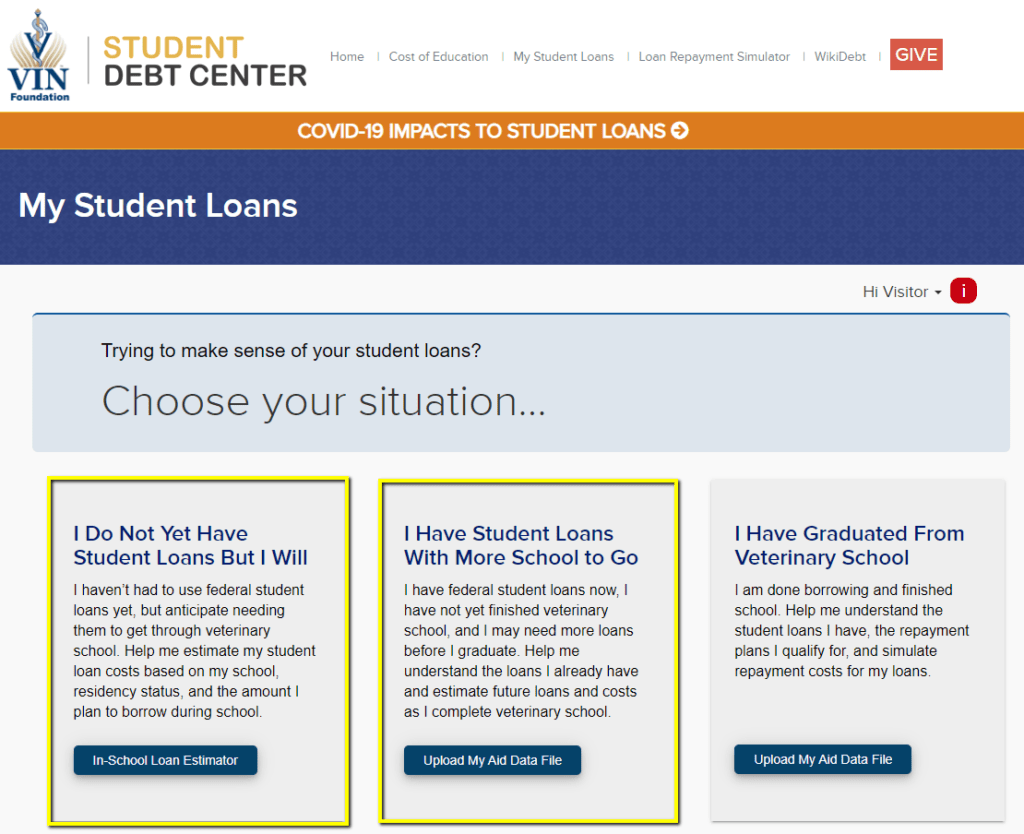

If you are starting veterinary school this fall or returning next fall, use the VIN Foundation My Student Loans tool and In-School Loan Estimator.

Here is a video tutorial on how to locate and download your student aid data file. These free tools help you account for loans you already have and help you estimate your total debt balance at graduation. You can even use the In-School Estimator to calculate how much you might save by returning unused student loans or reducing your future financial aid awards.

Less expensive options

Look for ways to borrow less expensive loans. Health Professions Student Loans (HPSL) and Loans for Disadvantaged Students (LDS) are potential federal alternatives to Direct loans for veterinary school if they are available for your education program and if you are eligible to receive them. HPSL and LDS have an interest rate of 5% and they do not accumulate interest during school (subsidized loans). They do, however, require you to provide your parents’ financial information in order to determine your eligibility. Check with your school financial aid office for more details on availability and the application process.

We’re here to help!

Happy budgeting this spring, summer, and fall. An ounce of planning is worth a pound of interest saved in repayment. Please feel free to reach out with any questions: [email protected]. VIN Foundation is here to help with understanding your veterinary school borrowing and repayment options now or in the future!