Skip to content

About

Story

Team

Get Involved

I am

An Animal Lover

Thinking of Being A Veterinarian

A Pre-Veterinary Student

A Veterinary Student

A New Veterinary Graduate

A Veterinarian

Programs

Apply Smarter

CE Courses

Cost of Education Toolkit

Disaster Relief

Dr. Sophia Yin Memorial Fund

Getting Through the Night / Day

I Want To Be A Veterinarian

Mike Dunn, DVM Veterinary Student Scholarship

Model Employment Contract

New Veterinary Graduate Survival Manual

Introduction

Where can I find tips on finding a job?

How can I create a terrific resume?

How can I create a great cover letter?

Do I need a contract?

How will I fit in veterinary medicine?

What is a mentor relationship?

How can I be the best mentee?

How can I be the best mentor?

What if I make mistakes?

Will it be an adventure?

Speaker Series

Startup Club

Student Debt

Student Debt Get Updates

Student Debt Center

Student Debt Help

2026 Summer Student Loan Guide

Download My IDR Progress Extension

Apply Smarter

40 Veterinary School Loan Estimations in 60 days

Borrow Better

Borrow Better Challenge

New Grad Playbook

Debt Repayment Prep Challenge

Interns/Residents/Specialists/Academics

Repay Wiser

Repayment Restart

Forgiveness Count Adjustment

Thrive In Five

Veterinary Pulse Podcast

Vets4Vets®

About Vets4Vets®

Connect with Vets4Vets®

CancerVets

ChallengeVets

Mentor Match

NAVLE Support

NeuroDivergent Vets

One on One

Online Weekly Meeting Groups

Peer Support

Support4Support

Team Trauma Triage

Veterinary Students

Vets in Recovery

Vet School Bound

Webinars

Contact

Get Updates

Blog

Nerdbook

Give

Annual Fund

Cor Group

Legacy Giving

Dr. Sophia Yin Memorial Fund

About

Story

Team

Get Involved

I am

An Animal Lover

Thinking of Being A Veterinarian

A Pre-Veterinary Student

A Veterinary Student

A New Veterinary Graduate

A Veterinarian

Programs

Apply Smarter

CE Courses

Cost of Education Toolkit

Disaster Relief

Dr. Sophia Yin Memorial Fund

Getting Through the Night / Day

I Want To Be A Veterinarian

Mike Dunn, DVM Veterinary Student Scholarship

Model Employment Contract

New Veterinary Graduate Survival Manual

Introduction

Where can I find tips on finding a job?

How can I create a terrific resume?

How can I create a great cover letter?

Do I need a contract?

How will I fit in veterinary medicine?

What is a mentor relationship?

How can I be the best mentee?

How can I be the best mentor?

What if I make mistakes?

Will it be an adventure?

Speaker Series

Startup Club

Student Debt

Student Debt Get Updates

Student Debt Center

Student Debt Help

2026 Summer Student Loan Guide

Download My IDR Progress Extension

Apply Smarter

40 Veterinary School Loan Estimations in 60 days

Borrow Better

Borrow Better Challenge

New Grad Playbook

Debt Repayment Prep Challenge

Interns/Residents/Specialists/Academics

Repay Wiser

Repayment Restart

Forgiveness Count Adjustment

Thrive In Five

Veterinary Pulse Podcast

Vets4Vets®

About Vets4Vets®

Connect with Vets4Vets®

CancerVets

ChallengeVets

Mentor Match

NAVLE Support

NeuroDivergent Vets

One on One

Online Weekly Meeting Groups

Peer Support

Support4Support

Team Trauma Triage

Veterinary Students

Vets in Recovery

Vet School Bound

Webinars

Contact

Get Updates

Blog

Nerdbook

Give

Annual Fund

Cor Group

Legacy Giving

Dr. Sophia Yin Memorial Fund

Search

Student Debt

Repayment Assistance Plan (RAP) Rules Finalized: Major unexpected change coming

Repayment Assistance Plan (RAP) Rules Finalized: Major unexpected change coming

Tony Bartels, DVM, MBA

•

May 6, 2026

•

Consolidation

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

VIN Foundation News

Urgent for Class of 2026: Do NOT Consolidate Your Federal Student Loans!

Urgent for Class of 2026: Do NOT Consolidate Your Federal Student Loans!

Tony Bartels, DVM, MBA

•

April 16, 2026

•

Consolidation

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

VIN Foundation News

VIN Foundation makes urgent call to Class of 2026 veterinary graduates, and those who advise them: Do NOT Consolidate. Student loan rules have changed, avoid this one critical mistake

VIN Foundation makes urgent call to Class of 2026 veterinary graduates, and those who advise them: Do NOT Consolidate. Student loan rules have changed, avoid this one critical mistake

VIN Foundation

•

April 15, 2026

•

Press Releases

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

VIN Foundation News

VIN Foundation Launches “40 Veterinary School Loan Estimations in 60 Days” to Help Future Veterinarians Navigate New Federal Student Loan Borrowing Limits

VIN Foundation Launches “40 Veterinary School Loan Estimations in 60 Days” to Help Future Veterinarians Navigate New Federal Student Loan Borrowing Limits

VIN Foundation

•

February 10, 2026

•

Press Releases

,

Veterinary Pre-Vets

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

VIN Foundation News

Federal Student Loan Repayment: 2025 Year-End Wrap and Preparing for 2026

Federal Student Loan Repayment: 2025 Year-End Wrap and Preparing for 2026

Tony Bartels, DVM, MBA

•

December 18, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Veterinary School: Private Student Loans vs. Federal Student Loans

Veterinary School: Private Student Loans vs. Federal Student Loans

Tony Bartels, DVM, MBA

•

November 20, 2025

•

Apply Smarter

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Fall 2025 Student Loan Borrow Better Challenge: Q&A

Fall 2025 Student Loan Borrow Better Challenge: Q&A

Tony Bartels, DVM, MBA

•

October 17, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Federal Health Professions Student Loans for Veterinary School

Federal Health Professions Student Loans for Veterinary School

Tony Bartels, DVM, MBA

•

September 30, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Changes to federal student loans come into focus

Changes to federal student loans come into focus

Tony Bartels, DVM, MBA

•

July 16, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Student Loan Repayment: Trying to leave the SAVE forbearance? Choose PAYE or Wait for RAP.

Student Loan Repayment: Trying to leave the SAVE forbearance? Choose PAYE or Wait for RAP.

Tony Bartels, DVM, MBA

•

July 11, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Student Loans in SAVE Plan Will Start Accruing Interest August 1st

Student Loans in SAVE Plan Will Start Accruing Interest August 1st

Tony Bartels, DVM, MBA

•

July 9, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

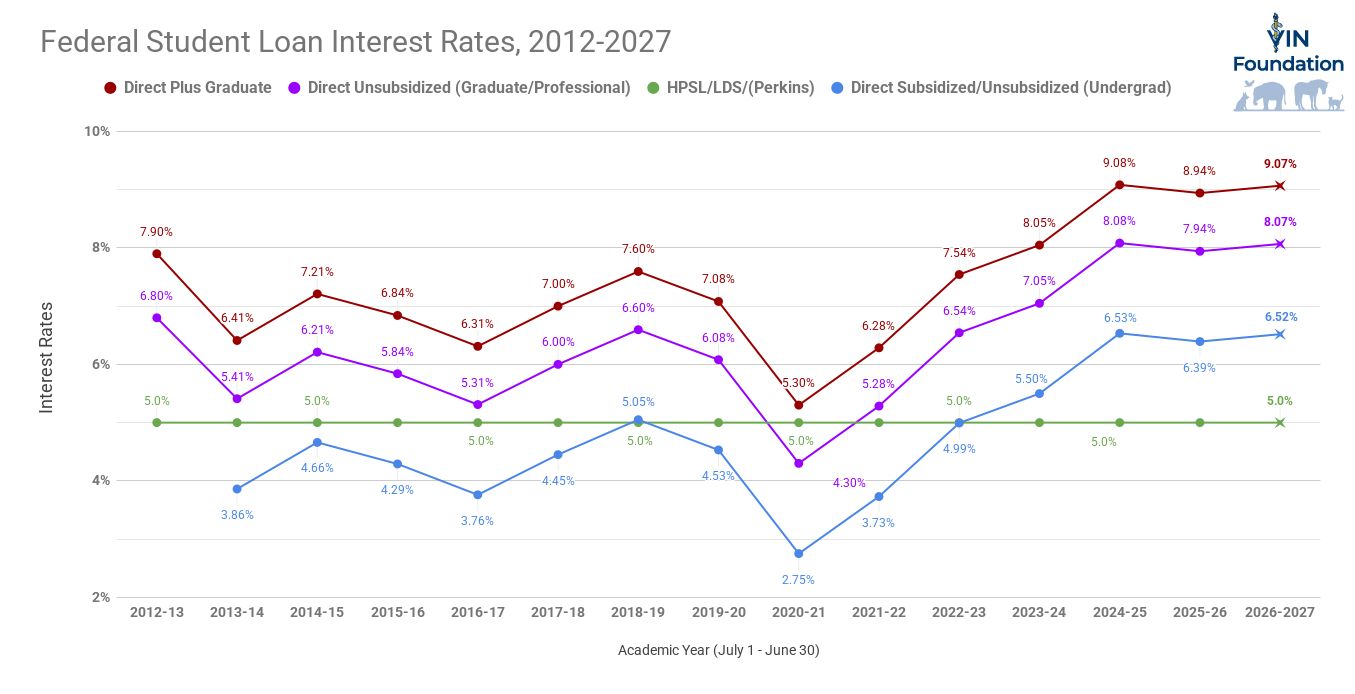

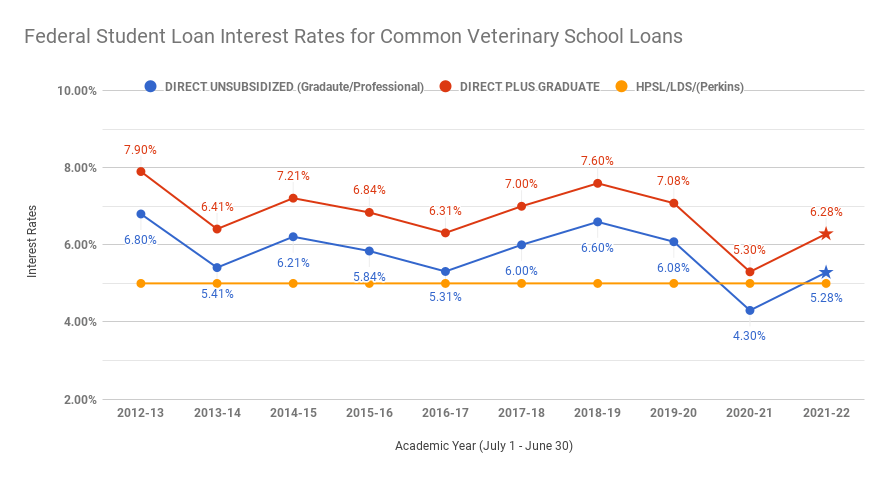

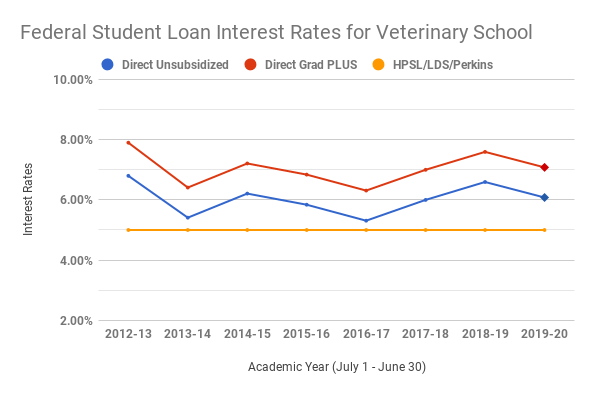

Student Loan Interest Rates Rise for 2026-2027 Academic Year

Student Loan Interest Rates Rise for 2026-2027 Academic Year

Tony Bartels, DVM, MBA

•

June 5, 2025

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Applying for a Repayment Plan

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Applying for a Repayment Plan

Tony Bartels, DVM, MBA

•

June 4, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Income-Driven Repayment Plans

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Income-Driven Repayment Plans

Tony Bartels, DVM, MBA

•

May 22, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

The Student Loan Consolidation Conundrum for 2025 New Graduates

The Student Loan Consolidation Conundrum for 2025 New Graduates

Tony Bartels, DVM, MBA

•

May 9, 2025

•

Consolidation

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Student Loan Grace Periods

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Student Loan Grace Periods

VIN Foundation

•

May 9, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics

VIN Foundation

•

May 9, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Student Loan Consolidation

2025 New Grad Student Loan Playbook: Live Session FAQ Hot Topics – Student Loan Consolidation

VIN Foundation

•

May 9, 2025

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Application for Federal Income-Driven Repayment Plans Reactivated

Application for Federal Income-Driven Repayment Plans Reactivated

Tony Bartels, DVM, MBA

•

March 28, 2025

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

All IDR applications for student loans are paused – Now what?

All IDR applications for student loans are paused – Now what?

Tony Bartels, DVM, MBA

•

February 28, 2025

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

February 2025 Q&A from Climbing Mt. Debt Webinar: What’s Next for your Student Loans?

February 2025 Q&A from Climbing Mt. Debt Webinar: What’s Next for your Student Loans?

Tony Bartels, DVM, MBA

•

February 7, 2025

•

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

How do new veterinary graduates really feel about their student debt?

How do new veterinary graduates really feel about their student debt?

VIN Foundation

•

January 22, 2025

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

,

VIN Foundation News

,

VIN Foundation Press

IDR Forgiveness Payment Count Data Available

IDR Forgiveness Payment Count Data Available

Tony Bartels, DVM, MBA

•

January 20, 2025

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

PAYE and ICR income-driven repayment plans temporarily reactivated

PAYE and ICR income-driven repayment plans temporarily reactivated

Tony Bartels, DVM, MBA

•

December 23, 2024

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

The election is over. Change is on the horizon. What is next for your student loans?

The election is over. Change is on the horizon. What is next for your student loans?

Tony Bartels, DVM, MBA

•

November 15, 2024

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

A Borrow Better Case Study Using the In-School Loan Estimator

A Borrow Better Case Study Using the In-School Loan Estimator

VIN Foundation

•

October 24, 2024

•

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

September 2024 Student Loan Update: FAQs and What’s Next?

September 2024 Student Loan Update: FAQs and What’s Next?

Tony Bartels, DVM, MBA

•

September 6, 2024

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

What do the recent court rulings on SAVE mean for you?

What do the recent court rulings on SAVE mean for you?

Tony Bartels, DVM, MBA

•

July 3, 2024

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

SECURE Act 2.0: Retirement plan contributions tied to your student loan payments

SECURE Act 2.0: Retirement plan contributions tied to your student loan payments

Tony Bartels, DVM, MBA

•

March 22, 2024

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Income-Driven Repayment: Recertify, Switch plans, or Wait?

Income-Driven Repayment: Recertify, Switch plans, or Wait?

Tony Bartels, DVM, MBA

•

March 13, 2024

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

2024 Graduating Veterinarians: Special Student Loan Timing Considerations

2024 Graduating Veterinarians: Special Student Loan Timing Considerations

Tony Bartels, DVM, MBA

•

February 16, 2024

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Choosing between PAYE and SAVE income-driven plans: Are you in The Pickle?

Choosing between PAYE and SAVE income-driven plans: Are you in The Pickle?

Tony Bartels, DVM, MBA

•

January 19, 2024

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

2026 Federal Poverty Rates Published: Why that matters for your student loans

2026 Federal Poverty Rates Published: Why that matters for your student loans

Tony Bartels, DVM, MBA

•

January 19, 2024

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Veterinary Student Loan Repayment: Trends from the trenches

Veterinary Student Loan Repayment: Trends from the trenches

Tony Bartels, DVM, MBA

•

November 1, 2023

•

Veterinary Questions & Answers

,

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Student Loan FAQs: The one-time forgiveness count adjustment

Student Loan FAQs: The one-time forgiveness count adjustment

Tony Bartels, DVM, MBA

•

September 1, 2023

•

Veterinary Questions & Answers

,

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Pandemic forbearance payments are eligible for a refund

Pandemic forbearance payments are eligible for a refund

VIN Foundation

•

August 25, 2023

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

I have federal student loans. When do I need to recertify my income?

I have federal student loans. When do I need to recertify my income?

Tony Bartels, DVM, MBA

•

June 1, 2023

•

Veterinary Questions & Answers

,

Veterinary Student Debt

,

Veterinary Student Loans

Student Debt Questions & Answers – from 3rd year veterinary students

Student Debt Questions & Answers – from 3rd year veterinary students

Tony Bartels, DVM, MBA

•

March 24, 2023

•

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

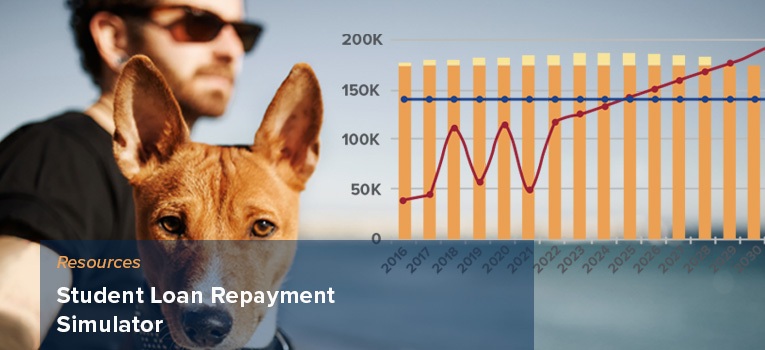

VIN Foundation Student Loan Repayment Simulator Adds Crucial Proposed Changes

VIN Foundation Student Loan Repayment Simulator Adds Crucial Proposed Changes

VIN Foundation

•

March 14, 2023

•

Press Releases

,

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

,

VIN Foundation News

A ‘new’ income-driven repayment plan?

A ‘new’ income-driven repayment plan?

Tony Bartels, DVM, MBA

•

February 7, 2023

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Comments to the Department of Education on proposed IDR changes

Comments to the Department of Education on proposed IDR changes

Tony Bartels, DVM, MBA

•

February 7, 2023

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

December 2022 Student Loan Update

December 2022 Student Loan Update

Tony Bartels, DVM, MBA

•

December 7, 2022

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Common Student Loan Consolidation Questions and Answers

Common Student Loan Consolidation Questions and Answers

Tony Bartels, DVM, MBA

•

November 1, 2022

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

VIN Foundation Student Debt Resources Updated to Address Latest Changes to Help Student Loan Forgiveness Strategies

VIN Foundation Student Debt Resources Updated to Address Latest Changes to Help Student Loan Forgiveness Strategies

VIN Foundation

•

October 25, 2022

•

Press Releases

,

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

,

VIN Foundation News

Class of 2020, 2021, 2022 Income-Driven Repayment Renewal Note

Class of 2020, 2021, 2022 Income-Driven Repayment Renewal Note

Tony Bartels, DVM, MBA

•

October 20, 2022

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Have you ever worked for a nonprofit? Act fast to benefit from the Limited PSLF Waiver

Have you ever worked for a nonprofit? Act fast to benefit from the Limited PSLF Waiver

Tony Bartels, DVM, MBA

•

September 22, 2022

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Special Cancellation of Up to $20,000 of Student Debt. Are You Eligible?

Special Cancellation of Up to $20,000 of Student Debt. Are You Eligible?

Tony Bartels, DVM, MBA

•

August 26, 2022

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

Got Federal Student Debt? You’re Now Closer to Forgiveness Than You Think

Got Federal Student Debt? You’re Now Closer to Forgiveness Than You Think

Tony Bartels, DVM, MBA

•

July 18, 2022

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

,

Veterinary Students

Student Loan Forgiveness Planning: Capital Gains Taxes

Student Loan Forgiveness Planning: Capital Gains Taxes

Tony Bartels, DVM, MBA

•

April 19, 2022

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

,

Veterinary Students

Federal Student Loan Repayment Pause Extended Again! Here is What You Need to Know…

Federal Student Loan Repayment Pause Extended Again! Here is What You Need to Know…

Tony Bartels, DVM, MBA

•

April 13, 2022

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Increase in Federal Poverty Rates for 2023: Why that matters for your student loans

Increase in Federal Poverty Rates for 2023: Why that matters for your student loans

Tony Bartels, DVM, MBA

•

February 2, 2022

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

FedLoan Servicing (PHEAA) to Stop Servicing Federal Student Loans

FedLoan Servicing (PHEAA) to Stop Servicing Federal Student Loans

VIN Foundation

•

July 13, 2021

•

Veterinary Student Debt

,

Veterinary Student Debt Relief

,

Veterinary Student Loans

,

VIN Foundation News

New Grad Student Loan Questions and Answers: Consolidation

New Grad Student Loan Questions and Answers: Consolidation

Tony Bartels, DVM, MBA

•

June 24, 2021

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

Webinars

Student Loan Interest Rates Increase for 2021-2022 Academic Year

Student Loan Interest Rates Increase for 2021-2022 Academic Year

Tony Bartels, DVM, MBA

•

June 1, 2021

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Sizing Up The Student Loan Forgiveness Tax Exemption

Sizing Up The Student Loan Forgiveness Tax Exemption

Tony Bartels, DVM, MBA

•

April 27, 2021

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

How Will the Pandemic Impact Early Veterinary Careers?

How Will the Pandemic Impact Early Veterinary Careers?

VIN Foundation

•

April 2, 2021

•

Veterinary Life

,

Veterinary Mental Health

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

Veterinary Wellness

Climbing Mt. Debt for SAVMA 2021

Climbing Mt. Debt for SAVMA 2021

VIN Foundation

•

March 30, 2021

•

Veterinary Presentations

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

Veterinary Videos

,

Webinars

Student Loan Forgiveness Planning: Preparing for the Tax Bill

Student Loan Forgiveness Planning: Preparing for the Tax Bill

Tony Bartels, DVM, MBA

•

December 15, 2020

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

COVID-19 Student Loan Repayment Restart

COVID-19 Student Loan Repayment Restart

Tony Bartels, DVM, MBA

•

December 8, 2020

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

The First Two Years of Student Loan Repayment for Veterinarians

The First Two Years of Student Loan Repayment for Veterinarians

Tony Bartels, DVM, MBA

•

November 12, 2020

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Saving Money in Veterinary School: Living Expenses

Saving Money in Veterinary School: Living Expenses

VIN Foundation

•

August 19, 2020

•

Veterinary Life

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Students

For the Aspiring Veterinarian – Apply Smarter!

For the Aspiring Veterinarian – Apply Smarter!

Tony Bartels, DVM, MBA

•

August 14, 2020

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

Apply Smarter Q&A: Vet School Application Questions

Apply Smarter Q&A: Vet School Application Questions

Tony Bartels, DVM, MBA

•

August 13, 2020

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Webinars

Apply Smarter Q&A: Student Loans and Financial Aid

Apply Smarter Q&A: Student Loans and Financial Aid

Tony Bartels, DVM, MBA

•

August 13, 2020

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Webinars

Apply Smarter Q&A: Veterinary Income

Apply Smarter Q&A: Veterinary Income

Tony Bartels, DVM, MBA

•

August 13, 2020

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Webinars

The Financials of Applying to Veterinary School – What I Wish I Had Known

The Financials of Applying to Veterinary School – What I Wish I Had Known

VIN Foundation

•

July 22, 2020

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Students

COVID-19 Impact to Your Student Loans

COVID-19 Impact to Your Student Loans

Tony Bartels, DVM, MBA

•

April 30, 2020

•

Veterinary Resources

,

Veterinary Student Debt

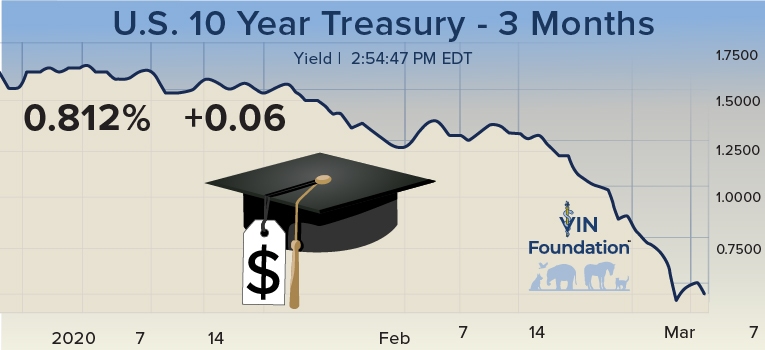

Should I Refinance My Federal Student Loans?

Should I Refinance My Federal Student Loans?

Tony Bartels, DVM, MBA

•

March 11, 2020

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Student Loan Forgiveness: Taxable or Tax-Free?

Student Loan Forgiveness: Taxable or Tax-Free?

Tony Bartels, DVM, MBA

•

February 12, 2020

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Employer Assisted Student Loan Repayment Benefits for Veterinarians

Employer Assisted Student Loan Repayment Benefits for Veterinarians

Tony Bartels, DVM, MBA

•

February 5, 2020

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Applying For or Renewing Your Income-Driven Repayment Plan

Applying For or Renewing Your Income-Driven Repayment Plan

Tony Bartels, DVM, MBA

•

December 24, 2019

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Apply Smarter Webinar in Collaboration with SDN and APVMA

Apply Smarter Webinar in Collaboration with SDN and APVMA

VIN Foundation

•

July 28, 2019

•

Apply Smarter

,

Press Releases

,

Veterinary Pre-Vets

,

Veterinary Presentations

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Webinars

How Income-Driven Repayment Works: The Rules

How Income-Driven Repayment Works: The Rules

Tony Bartels, DVM, MBA

•

July 24, 2019

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

How Income-Driven Repayment Works: The Math

How Income-Driven Repayment Works: The Math

Tony Bartels, DVM, MBA

•

July 23, 2019

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

New Grad Student Loan Questions and Answers: Income-Driven Repayment (PAYE, REPAYE, IBR)

New Grad Student Loan Questions and Answers: Income-Driven Repayment (PAYE, REPAYE, IBR)

Tony Bartels, DVM, MBA

•

June 5, 2019

•

Consolidation

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Repay Wiser: 2019 New Veterinary Graduate Student Loan Playbook

Repay Wiser: 2019 New Veterinary Graduate Student Loan Playbook

Tony Bartels, DVM, MBA

•

May 13, 2019

•

Consolidation

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

Webinars

Lower Student Loan Interest Rates for 2019

Lower Student Loan Interest Rates for 2019

Tony Bartels, DVM, MBA

•

May 9, 2019

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Top 5 Mistakes Made by Veterinarians Using Income-Driven Repayment

Top 5 Mistakes Made by Veterinarians Using Income-Driven Repayment

Tony Bartels, DVM, MBA

•

March 20, 2019

•

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Veterinary Student Debt Questions and Answers Part 2

Veterinary Student Debt Questions and Answers Part 2

Tony Bartels, DVM, MBA

•

March 19, 2019

•

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Furloughed and Unpaid Federal Veterinarians

Furloughed and Unpaid Federal Veterinarians

Tony Bartels, DVM, MBA

•

January 28, 2019

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

In-School Loan Estimator expands VIN Foundation Student Debt Center

In-School Loan Estimator expands VIN Foundation Student Debt Center

VIN Foundation

•

January 17, 2019

•

Press Releases

,

Veterinary Student Debt

,

VIN Foundation News

Veterinary Student Debt Questions and Answers

Veterinary Student Debt Questions and Answers

Tony Bartels, DVM, MBA

•

December 16, 2018

•

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Student Loan Interest Rates and Repayment — Don’t Listen to Your Parents!

Student Loan Interest Rates and Repayment — Don’t Listen to Your Parents!

Paul D. Pion, DVM, DipACVIM (Cardiology)

•

August 27, 2018

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

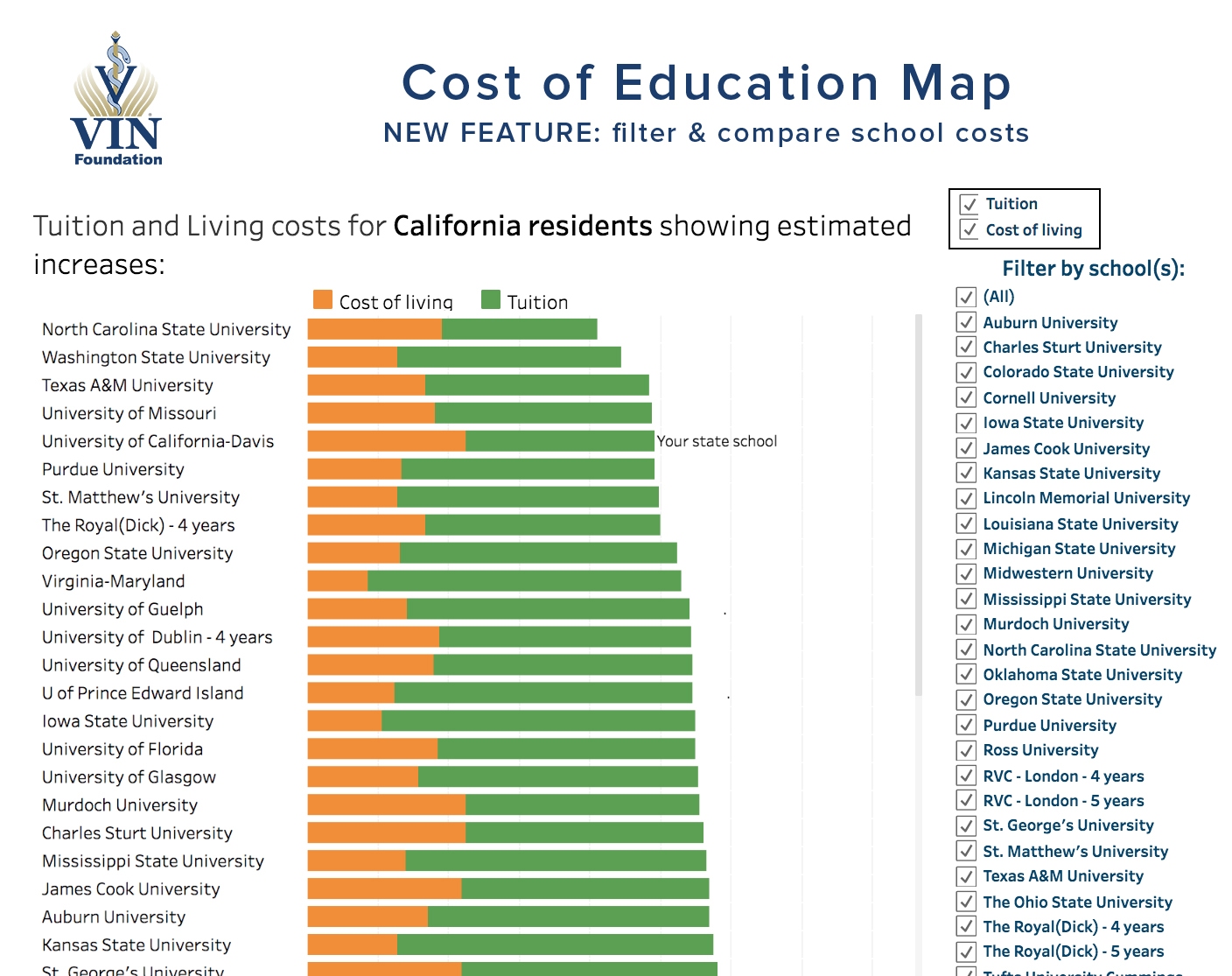

Exciting Enhancements to Veterinary Cost of Education Map

Exciting Enhancements to Veterinary Cost of Education Map

VIN Foundation

•

August 15, 2018

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Students

Choosing the Best Veterinary School for You

Choosing the Best Veterinary School for You

Tony Bartels, DVM, MBA

•

June 27, 2018

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

2018 New Veterinary Graduate Student Loan Playbook

2018 New Veterinary Graduate Student Loan Playbook

Tony Bartels, DVM, MBA

•

June 1, 2018

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

,

Webinars

Student Loan Interest Rates Increasing

Student Loan Interest Rates Increasing

Tony Bartels, DVM, MBA

•

May 22, 2018

•

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Sharing Saves Time, Income-Driven Repayment Saves Money

Sharing Saves Time, Income-Driven Repayment Saves Money

Tony Bartels, DVM, MBA

•

March 21, 2018

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

Estimate Your Minimum Monthly Student Loan Payment

Estimate Your Minimum Monthly Student Loan Payment

Tony Bartels, DVM, MBA

•

January 30, 2018

•

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

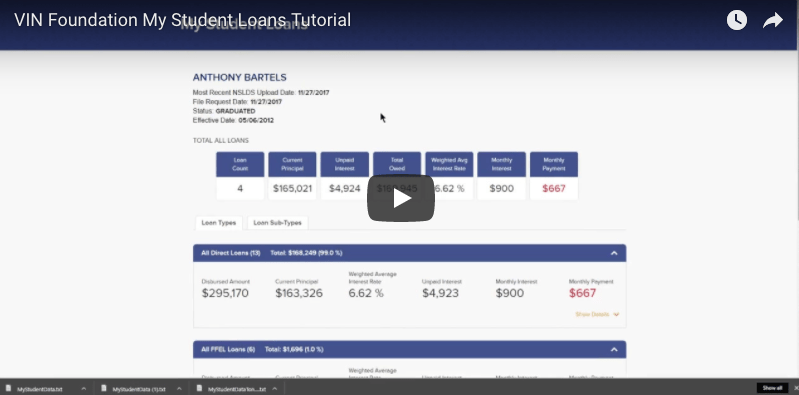

My Student Loans

My Student Loans

Tony Bartels, DVM, MBA

•

November 30, 2017

•

Veterinary Student Debt

,

Veterinary Student Loans

,

Veterinary Students

Veterinary School Class Recommendations

Veterinary School Class Recommendations

VIN Foundation

•

November 2, 2017

•

Apply Smarter

,

Veterinary Pre-Vets

,

Veterinary Questions & Answers

,

Veterinary Resources

,

Veterinary School

,

Veterinary Student Debt

,

Veterinary Students

Veterinary Student Debt Center Launches

Veterinary Student Debt Center Launches

VIN Foundation

•

March 14, 2017

•

Veterinary Resources

,

Veterinary Student Debt

,

Veterinary Student Loans

,

VIN Foundation News

Blog Topics

VIN Foundation News

Mental Health

Student Debt

Questions & Answers

Apply Smarter

Veterinary Students

Webinars

All Blog Posts

VIN Foundation News

Mental Health

Student Debt

Questions & Answers

Apply Smarter

Veterinary Students

Webinars

All Blog Posts

Scroll to Top