Think of switching plans and recertifying your income as two separate events. In fact, there are different options for you to select if you are recertifying your income vs. switching repayment plans on StudentAid.gov/idr as show in the image below.

It might make sense for you to switch plans and you might be waiting to switch until you’re due to renew. Let’s consider a case where a recent graduate has a very low payment using PAYE but has decided SAVE will be a better plan for them. They want to keep the favorable PAYE payment for as long as possible, then switch to SAVE as their favorable PAYE payment expires. Switching repayment plans during your renewal period is a great time to switch plans. However, leave yourself enough time for your switch to process. If your application to switch is not processed before your Anniversary Date, then you could end up in forbearance with interest accruing or seeing one of those fixed 10-year plan payment statements issued.

Unlike renewing or recertifying your existing income-driven plan, your new payment schedule will start as soon as your application to switch is processed. Unfortunately, it’s impossible to say how long your application to switch will take given poor loan servicer performance as repayment has restarted.

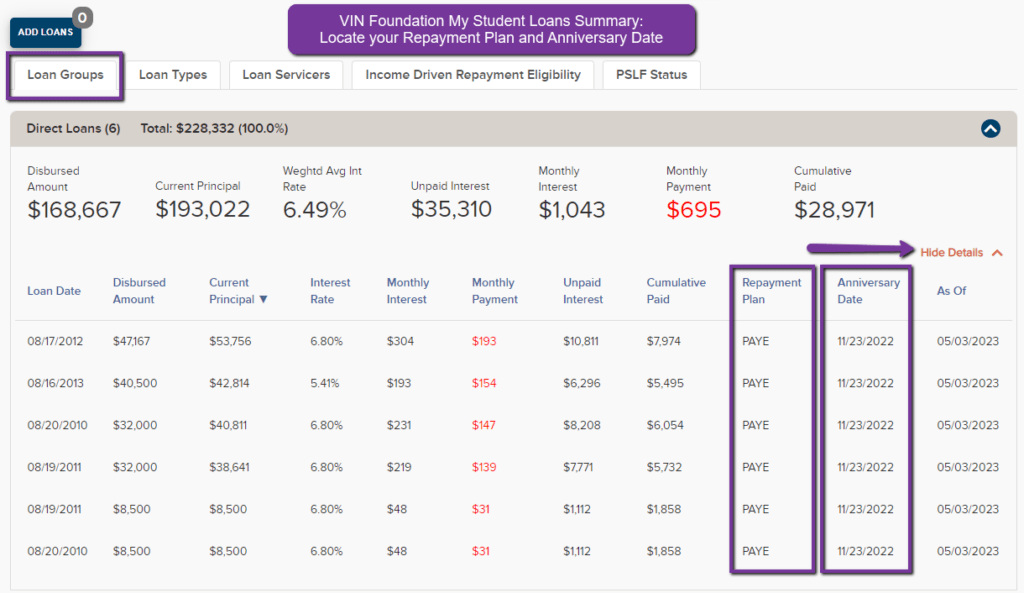

You can try to make the most out of your time with a previously lower payment but don’t wait too long. Oftentimes, borrowers think they don’t need to renew until their Anniversary Date. Unfortunately, your Anniversary Date is your expiration date. You must provide income information before your Anniversary Date to continue having a payment that is calculated from your income.

Dr. Tony Bartels graduated in 2012 from the Colorado State University combined MBA/DVM program and is an employee of the Veterinary Information Network (VIN) and a VIN Foundation Board member. He and his wife have more than $400,000 in veterinary-school debt that they manage using federal income-driven repayment plans. By necessity (and now obsession), his professional activities include researching and speaking on veterinary-student debt, providing guidance to colleagues on loan-repayment strategies and contributing to VIN Foundation initiatives.

1 thought on “I have federal student loans. When do I need to recertify my income?”

My anniversary date is October 24,2023. So my new date would be October 24, 2024?