2026 New Graduate Student Loan Playbook Webinar: 4/22 5pm PT

Major unexpected repayment rule change impacting student loan forgiveness

On Thursday, April 30, 2026, the Department of Education finalized the Reimaging and Improving Student Education (RISE), aka the new borrowing and repayment rules for implementing the legislative updates for the Higher Education Act in the One Big Beautiful Bill signed on July 4, 2025: https://public-inspection.federalregister.gov/2026-08556.pdf.

There is one major unexpected change to the repayment rules in this final version that conflicts with the repayment recommendations made during the recent New Graduate Student Loan Repayment Playbook webinar and those looking towards the new Repayment Assistance Plan (RAP) as their next repayment option:

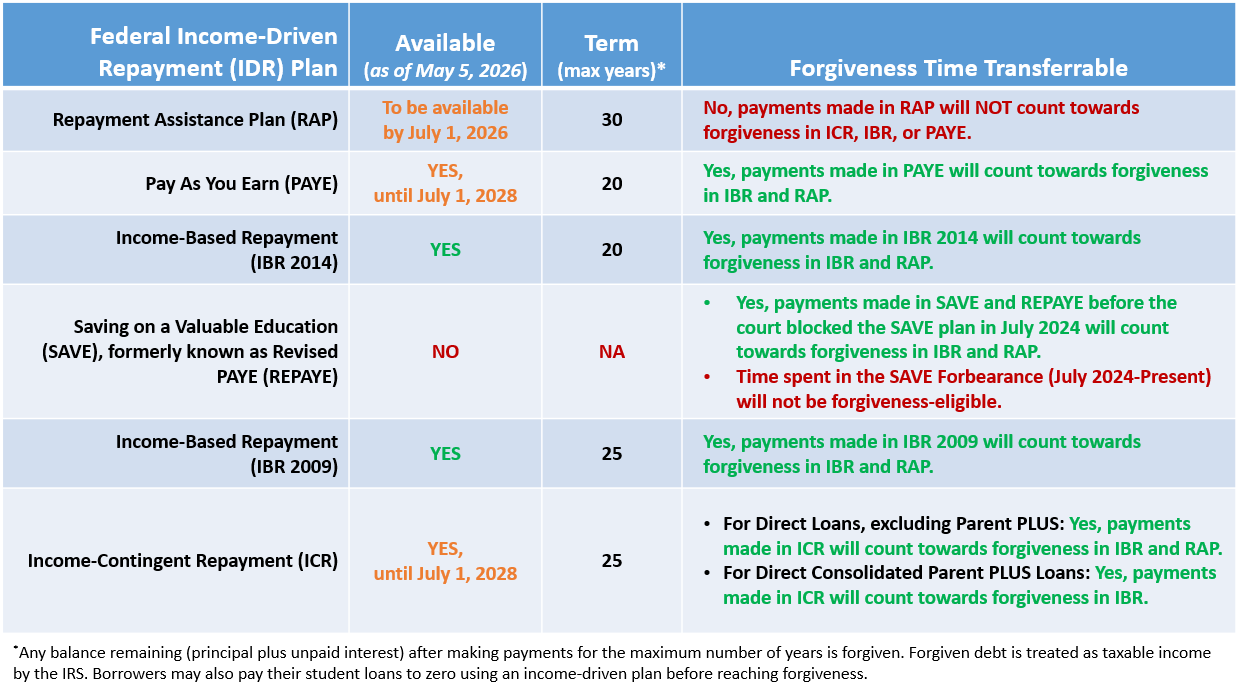

Payments made in the new RAP income-driven plan will NOT count towards Income-Based Repayment (IBR), Pay-As-You-Earn (PAYE), or Income-Contingent Repayment (ICR) forgiveness, collectively referred to now as the legacy income-driven repayment (IDR) plans. However, as expected, payments made in IBR, PAYE, or ICR will count towards RAP forgiveness.

This rule change will impact repayment plan recommendations for those who are eligible for legacy IDR options (IBR, PAYE, ICR) and the new RAP option. Read more to see how this new change will impact your repayment strategy, depending on your IDR Profile (a VIN Foundation determination of your eligible income-driven repayment plans based on your student loan borrowing history), your student debt-to-income ratio, and how many years you have been in repayment.

WikiDebt: What is your IDR Profile?

Your IDR eligibility is determined by your loan types and borrowing history. With ambiguous criteria and changing rules, one of the most difficult aspects of federal student loan repayment is knowing which repayment options are available for your loans. The VIN Foundation My Student Loans tool attempts to clarify the confusion and provide a simplified description of your IDR eligibility via the IDR Profile.

There are six different VIN Foundation IDR Profiles:

- IDR Profile 1: Eligible for ICR, PAYE, and IBR 2014, and RAP**

- IDR Profile 2: Eligible for ICR, IBR 2009, PAYE, and RAP**

- IDR Profile 3: Eligible for ICR, IBR 2009, and RAP**

- IDR Profile 4: Eligible for IBR 2009 only

- IDR Profile 5: Eligible for ICR only

- IDR Profile 6: Eligible for RAP** only (coming soon…)

See the WikiDebt IDR Profiles page for more details.

VIN Foundation My Student Loans tool

Rule Change Impact for 2026 new graduate veterinarian in IDR Profile 1:

New graduates (Class of 2026) should still avoid federal Direct Consolidation of their federal student loans to preserve access to IBR. Most new graduates will be eligible for IBR 2014, along with the new RAP option. Having access to both plans gives new graduates repayment flexibility regardless of their post-graduation career path.

New graduates may benefit from starting with RAP for the low monthly payment, 100% unpaid interest subsidy, and $50/month principal credit while your RAP payment is less than your monthly interest accrual. However, under the recently finalized repayment rules, RAP payments will count towards the 30 years of payments required to reach forgiveness in RAP, but RAP forgiveness credit will not transfer to IBR 2014 if/when you switch from RAP to IBR 2014.

Alternatively, a new graduate could start with IBR 2014 and forgo RAP. This could be the most direct and inexpensive pathway to student loan forgiveness at 20 years, or Public Service Loan Forgiveness (PSLF) at 10 years. Monthly minimum payments due in IBR 2014 are generally lower than RAP, particularly once your Adjusted Gross Income (AGI) exceeds $80,000. Forgiveness is reached in IBR 2014 after 20 years of qualifying payments vs. 30 years in RAP. Generally, the shorter the maximum repayment time, the less you will pay. However, unlike RAP, IBR 2014 does not have an unpaid interest subsidy nor a principal reduction while your payment is less than the monthly interest accrual.

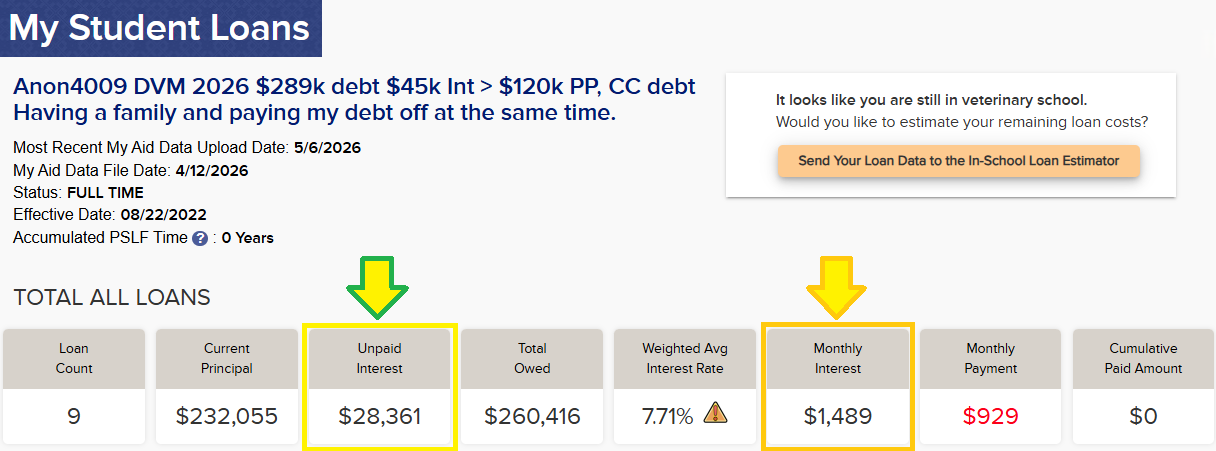

Most new graduates will enter federal student loan repayment with an unpaid interest balance – the interest that accrued during veterinary school. Most new graduates can also apply for RAP or IBR 2014 using their 2025 federal income tax return AGI. This will result in a minimum payment that is less than your monthly student loan interest accrual, aka negative amortization. In IBR, the interest not covered by your monthly payment will be added to your separate unpaid interest “bucket.” Interest does not accrue on this separate “bucket.” But federal law requires this unpaid interest to be paid down before payments start to impact your principal. Thus, your unpaid interest balance can grow while using IBR 2014 compared to RAP.

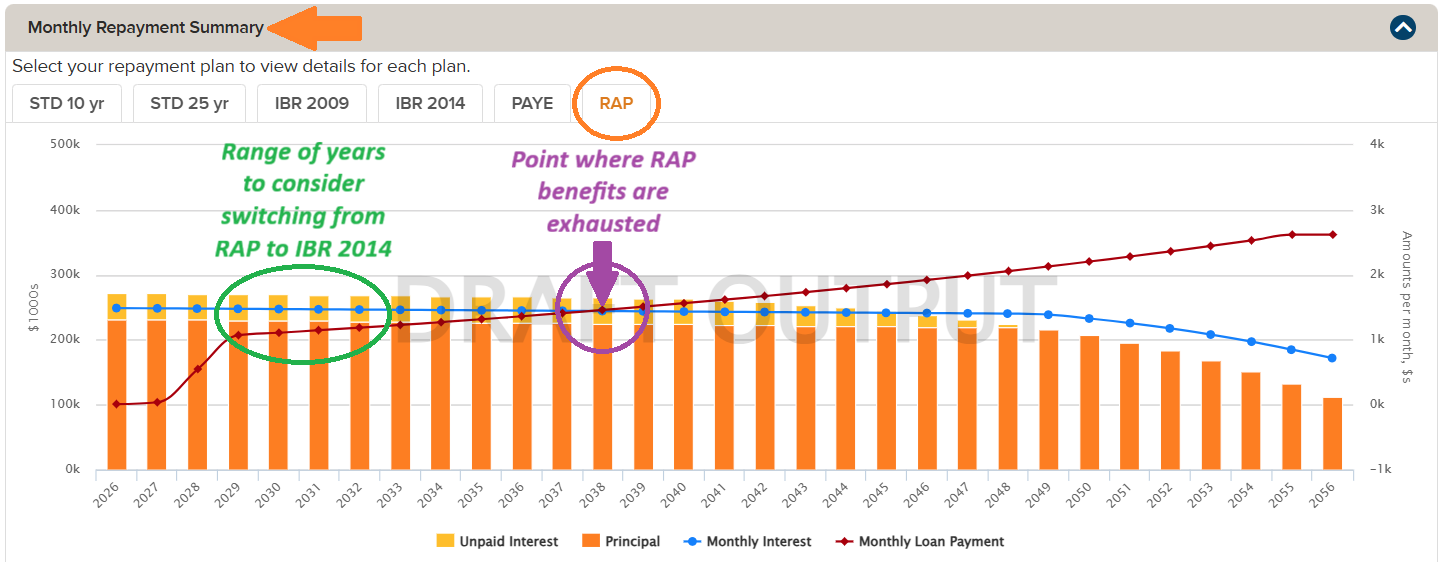

Showing Unpaid Interest and Monthly Interest Accrual

Those heading into internship or residency training will want to use the new RAP option to prevent their unpaid interest balance from growing and to ensure their balance decreases for the duration of their training. After completing your additional training, re-evaluate your repayment strategy to see if it makes sense to switch to IBR 2014, stick with RAP, or something else.

As we discussed in the recent Playbook webinar, new grads can still use a strategic combination of RAP and IBR 2014 to reach forgiveness sooner and lower their total repayment costs. For example, a new graduate veterinarian with a starting student debt-to-income ratio greater than 2 could use RAP for the first few years of repayment to receive the subsidy benefit, then switch to IBR 2014 to receive forgiveness 20 years after entering IBR 2014. Using RAP for the first 3 years of repayment, then switching to IBR 2014, would reach forgiveness after 23 years of repayment. While not as beneficial as the draft RAP repayment rules, starting with RAP and then switching to IBR 2014 will help you receive the subsidy benefits of RAP in the early years of repayment and reach forgiveness sooner, with lower long-term payments and a monthly payment cap provided by IBR 2014.

VIN Foundation Student Loan Repayment Simulation for 2026 DVM:

- Starting repayment balance: $232,055 Principal at 7.71% with $40,238 Unpaid Interest after Grace Period ends

- Starts with an internship earning $45,000/yr

- Private Practice after internship with $120,000/yr

- Link to Simulation

For most 2026 new graduate veterinarians, you will pay very little towards your student loans in at least the first 2 years of repayment using RAP. Therefore, switching from RAP to IBR 2014 to reach forgiveness 20 years after entering IBR 2014 will not appreciably increase your total repayment costs, but it does give you a couple of years after graduation to boost your financial wellness and learn more about your income and financial needs.

The most challenging repayment scenarios will be those who would benefit from the RAP subsidies for up to 10 years after graduation. Under the recently finalized rules, switching to IBR 2014 after using RAP for 10 years will keep you in repayment for 30 years total, even if you reach forgiveness in IBR 2014 (10 years in RAP plus 20 years maximum in IBR 2014). For those scenarios, it may make more sense to stick with RAP for the duration or repayment or find a time to switch from RAP to IBR 2014 before making 10 years of payments in RAP.

In the coming weeks, the new finalized rules will be integrated into the VIN Foundation Student Loan Repayment Simulations to help you (and all of us) better understand your long-term repayment costs.

2026 DVM in IDR Profile 1: Why not start with IBR 2014?

You can, but starting with IBR comes with some risk. In many cases, using IBR 2014 for 20 years will be the cheapest way to eliminate your federal student debt. However, if you start with IBR and then leave IBR, your unpaid interest capitalizes, i.e., gets added to your principal, thereby increasing your principal balance and increasing the amount of interest that accrues on your loans each month. The more interest accrues, the more you will pay over time (unless you reach PSLF). For this reason, it makes more sense to start with RAP, then switch to IBR 2014. If you start with IBR 2014 and later decide you could benefit from RAP, you will capitalize the unpaid interes from veterinary school and any additional unpaid interest that has accrued in repayment. If you can help it, select IBR 2014 when you are ready for that to be your final repayment plan.

2026 new graduate veterinarian in IDR Profile 2:

New graduates (Class of 2026) should still avoid federal Direct Consolidation of their federal student loans to preserve access to IBR. While most new graduates will be eligible for IBR 2014, those in IDR Profile 2 are still eligible for IBR 2009, along with the new RAP option. Having access to both plans gives new graduates repayment flexibility regardless of their post-graduation career path.

If you’re in IDR Profile 2 as a new graduate, we will need your help to work through these situations in a bit more detail on the Student Debt Message Boards to see which combination of plan(s) will work best given your student debt-to-income ratio, career plans, income, and family situation.

PAYE will be available as a repayment option until July 1, 2028. Payments made using PAYE will be eligible for forgiveness in the legacy IDR plans. However, after July 1, 2028, those using PAYE will need to select either IBR 2009 or RAP as their new income-driven repayment plan. Both remaining options for those in IDR Profile 2 have a longer time to reach forgiveness (IBR 2009: 25 years; RAP: 30 years) compared to PAYE (20 years).

IBR 2009 would be the most direct path to reach forgiveness after PAYE. You will need to simulate your repayment to see if you are still projected to reach forgiveness in IBR 2009 after PAYE is eliminated.

Your legacy IDR forgiveness credit will count towards forgiveness in RAP, but RAP requires 30 years of total repayment time to reach forgiveness. You can also consider using RAP temporarily to navigate a low-income situation; however, the new rules will not allow RAP payments to count towards legacy IDR forgiveness if you switch out of RAP into IBR 2009 in the future. That doesn’t mean you shouldn’t use RAP if you need it; it just means you’ll be in repayment longer if you are projected to reach forgiveness.

2026 new graduate veterinarian heading for PSLF

Payments to federal student loans made using PAYE, IBR, or RAP while meeting the employment requirements for PSLF will count towards the 120 monthly payments needed to be eligible for PSLF. In general, to maximize the benefit of PSLF, choose the option with the lowest minimum monthly payment that is PSLF-eligible.

However, for those who are not sure if they will continue in PSLF-eligible employment for 10 years, RAP is a great hedge to keep your payments low and prevent your balance from decreasing (while receiving the RAP subsidies). If you start with RAP, then switch gears away from PSLF later, you will have a lower balance to manage through the remainder of repayment.

Veterinarians graduated prior to 2026: Check your IDR forgiveness progress

For those who are already in repayment and who are evaluating if RAP will be useful for your situation, first check your IDR forgiveness progress. Right now, that is only available through a “backdoor” API accessible after first logging in to studentaid.gov: https://studentaid.gov/app/api/nslds/payment-counter/summary

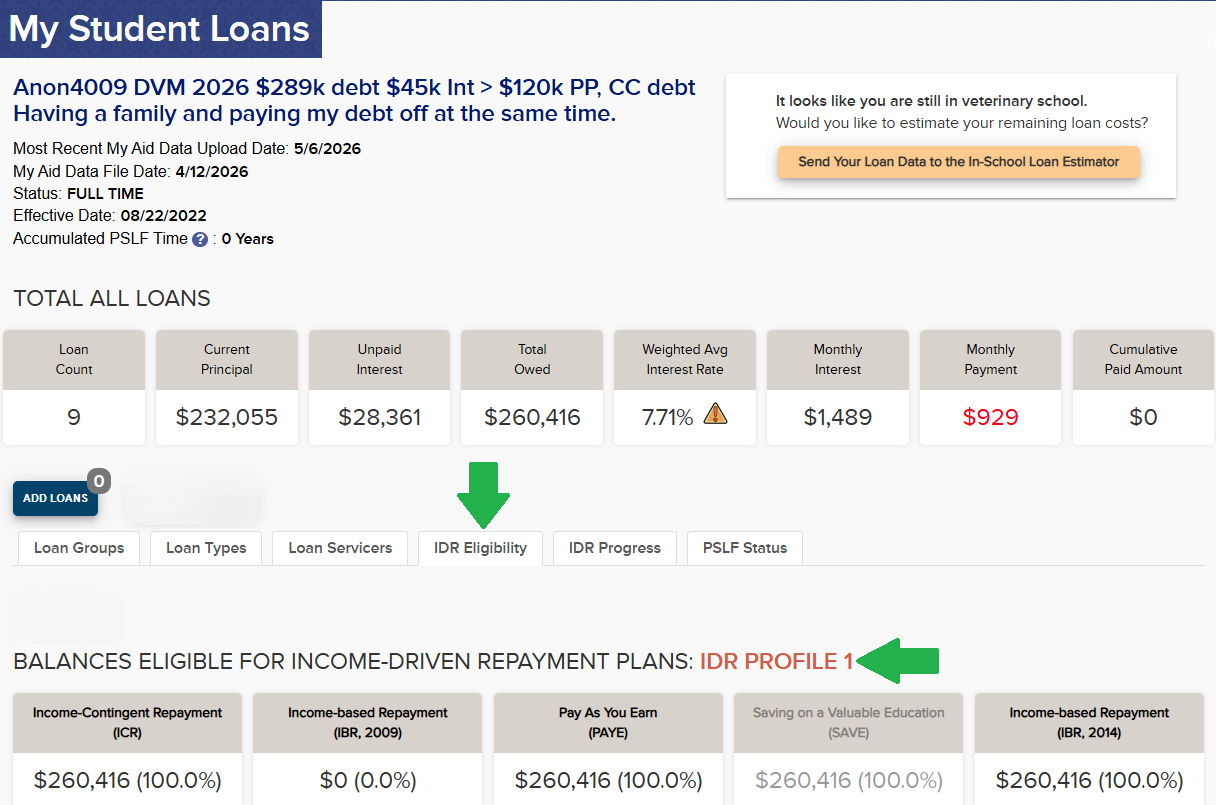

After checking your forgiveness progress, check your IDR Profile in the VIN Foundation My Student Loans tool:

- Step 1) Download your student aid data file from studentaid.gov

- Step 2) Upload your student aid file to VIN Foundation My Student Loans

- Step 3) Check the IDR Eligibility tab to see your IDR Profile.

Once you know your IDR Profile, check your current repayment plan status. If you’re using a plan like PAYE or IBR, check your income-driven repayment plan’s “Anniversary Date.” You will need to provide updated income information at least 35 days before your IDR Anniversary Date.

For those in the SAVE Forbearance, your Anniversary Date is meaningless. SAVE has been officially eliminated through a recently approved settlement of the litigation that blocked the SAVE plan. According to the Department of Education, anyone in the SAVE Forbearance will need to select a new repayment option within 90 days of being notified by your loan servicer. You can see your loan servicer information in your My Student Loans summary, too.

After checking your IDR forgiveness progress, IDR Profile, IDR Anniversary Date, check your monthly interest accrual. Is your current IDR payment less than or more than your monthly interest accrual? What would your RAP payment be? Are you projected to reach forgiveness in your remaining eligible IDR legacy plans or RAP? The answers to these question will help you determine what you should do with your student loans in the short and long-term. Read more for continued guidance on specific IDR Profiles.

Veterinarians graduated prior to 2026: IDR Profile 1

You may benefit from moving or keeping your loans in IBR 2014, especially if you’re projected to reach forgiveness after 20 years of qualifying payments. Unfortunately, under the finalized rules, payments made in the new RAP option will not count towards your 20 years of qualifying payments to reach forgiveness in IBR 2014. However, if you could benefit from the RAP subsidies in the short-term, then consider switching to RAP to prevent your interest from growing and to reduce your principal, then switch to IBR 2014 to continue your progress towards forgiveness after 20 years of qualifying payments in IBR 2014.

To hedge your bets, if you’re not already in IBR 2014, you could use PAYE until it is eliminated on July 1, 2028. PAYE will have the same payment as IBR 2014. The benefit of PAYE over IBR 2014 is not having your unpaid interest capitalized when you leave PAYE. Thus, if you want a couple more years to see if you may want to use RAP, then use PAYE while it is available.

Veterinarians graduated prior to 2026: IDR Profile 2

Utilize PAYE until it is eliminated on July 1, 2028.

If you are projected to reach forgiveness using IBR 2009, then switch from PAYE to IBR 2009 after PAYE is eliminated, pay the minimum in IBR 2009, and plan for the tax on forgiveness.

If you are not projected to reach forgiveness in IBR 2009, then consider switching to RAP to pay your loans to zero before reaching forgiveness. If it’s not clear whether or not you will reach forgiveness, then select IBR 2009 after PAYE is eliminated, just in case your situation changes in the future and you do end up reaching forgiveness. It’s better to earn forgiveness credit and not need it than to forgo forgiveness credit and find out later that you could have used it.

In general, if your income is less than your remaining student loan balance, then you could benefit from RAP. However, payments made in RAP will not count towards the 25 years of qualifying payments needed to reach forgiveness under ICR or IBR 2009. But, prior payments in ICR, IBR 2009, REPAYE, or SAVE do count towards the 30 years of qualifying payments needed to reach RAP forgiveness. Thus, if you have a relatively high student debt-to-income ratio and could benefit from the RAP subsidies or extra time to forgiveness, consider moving to RAP and riding it out until you either pay your balance to zero or reach student loan forgiveness.

Veterinarians graduated prior to 2026: IDR Profile 3

ICR or IBR 2009 is likely your best option, particularly if you are nearing forgiveness at 25 years. Once again, if you haven’t checked your IDR forgiveness progress, do so before you change your repayment strategy. You could be much closer to student loan forgiveness than you realize. We have seen a number of veterinarians who have been in repayment for 20 or more years recently receive student loan forgiveness. You may simply need to get your loans into a forgiveness-eligible IDR plan.

If your income is less than your remaining student loan balance, then you may benefit from RAP. However, under the recently finalized rules, payments made in RAP will not count towards the 25 years of qualifying payments needed to reach forgiveness using ICR or IBR 2009. But, prior payments in ICR, IBR 2009, REPAYE, or SAVE do count towards the 30 years of qualifying payments needed to reach RAP forgiveness. Thus, if you have a relatively high student debt to income ratio and could benefit from the RAP subsidies or extra time to forgiveness, consider moving to RAP and riding it out until you either pay your balance to zero or reach student loan forgiveness after a total of 30 years of qualifying IDR payments.

Veterinarians graduated prior to 2026: Heading for PSLF

Choose the income-driven plan that has the lowest monthly payment available for your IDR Profile. All payments made using an income-driven plan are qualifying payments for PSLF. Check your PSLF progress and apply for PSLF after reaching 120 qualifying monthly payments. Student loan forgiveness received under PSLF is tax-free.

Need student loan help?

Have more questions? Post a comment below or email [email protected].

We’re here to help!

Dr. Tony Bartels graduated in 2012 from the Colorado State University combined MBA/DVM program and is an employee of the Veterinary Information Network (VIN) and a VIN Foundation Board member. He and his wife have more than $400,000 in veterinary-school debt that they manage using federal income-driven repayment plans. By necessity (and now obsession), his professional activities include researching and speaking on veterinary-student debt, providing guidance to colleagues on loan-repayment strategies and contributing to VIN Foundation initiatives.