2026 New Graduate Student Loan Playbook Webinar: 4/22 5pm PT

RAP UPDATE ALERT:

Final borrowing and repayment rules were published in the Federal Register on May 1, 2026.

There is one major unexpected change to repayment rules in this final version:

Payments made in the new Repayment Assistance Plan (RAP) will NOT count towards legacy income-driven repayment (IDR) plan forgiveness (IBR, PAYE, or ICR). However, as expected, payments made in IBR, PAYE, or ICR will count towards RAP forgiveness.

What is IDR plan forgiveness? IDR plans require you to make a minimum monthly payment calculated from your income. You update your income information and have your payment recalculated at least annually. You will either reach a zero balance or reach the maximum number of years allowed in your IDR plan (20-30 years, depending on your IDR eligibility). If you reach the maximum number of years for your IDR plan and still have a balance, the remaining balance is forgiven. Forgiven debt is normally treated as taxable income, so you will likely incur a federal (and possibly state) tax on your forgiven balance.

DVM/VMD Class of 2026

Do NOT consolidate your federal student loans!

What is student loan consolidation? Consolidating your loans, by definition, means replacing one or more loans with a single new loan. For federal student loans, applying for a federal Direct Consolidation Loan replaces some or all eligible federal student loans with a new loan, named a Direct Consolidation Loan. The resulting interest rate for the consolidation loan is a weighted average of all the loans included in the consolidation.

Receiving any new Direct Loan (even a Direct Consolidation Loan) on July 1, 2026, or later will limit your federal repayment options to the new Repayment Assistance Plan (RAP) and tiered Standard Plan options.

It will be logistically improbable for most 2026 graduates to get a federal Direct Consolidation loan application processed and received before July 1, 2026.

For example, many new veterinarians graduate in early to mid-May 2026. Even if you start your Direct Consolidation Loan application the day after you graduate (presuming your loans allow you to do so), that leaves you about 45 days for the application to be processed and your new Direct Loan Consolidation to be received before July 1, 2026.

Consolidation applications take 30-60 days to complete in the best of times. It is too risky to hope that your consolidation will be completed by July 1st.

Why should the Class of 2026 avoid consolidation?

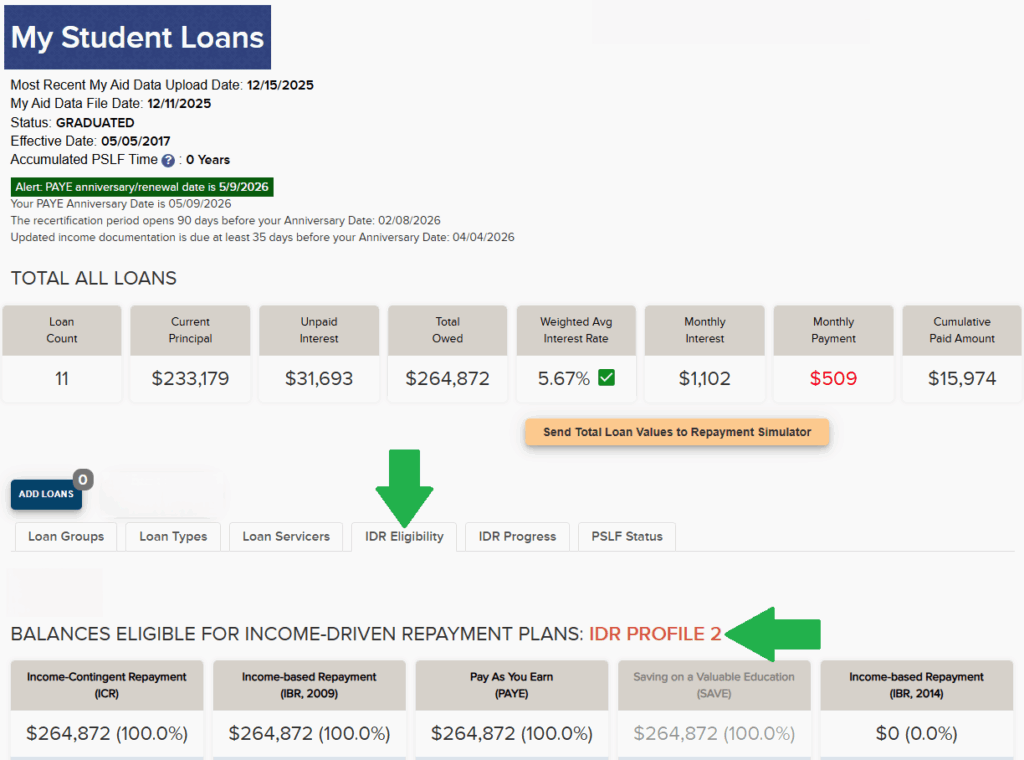

The class of 2026 will be the last graduating veterinarians eligible for the “legacy” income-driven repayment (IDR) plans, depending on their borrowing history. Use the VIN Foundation My Student Loans tool to check your IDR Profile.

Legacy IDRs include the Income-Contingent Repayment (ICR), Pay-As-You-Earn (PAYE), and Income-Based Repayment (IBR) plans.

IBR is particularly beneficial as it provides a monthly payment cap and a 20-year forgiveness option for anyone who received their first Direct Loan after July 1, 2014, and does not receive a loan on or after July 1, 2026.

WikiDebt: What is your IDR Profile?

Your IDR eligibility is determined by your loan types and borrowing history. With ambiguous criteria and changing rules, one of the most difficult aspects of federal student loan repayment is knowing which repayment options are available for your loans. The VIN Foundation My Student Loans tool attempts to clarify the confusion and provide a simplified description of your IDR eligibility via the IDR Profile.

There are six different VIN Foundation IDR Profiles:

- IDR Profile 1: Eligible for ICR, PAYE, and IBR 2014, and RAP (once available)

- IDR Profile 2: Eligible for ICR, IBR 2009, PAYE, and RAP (once available)

- IDR Profile 3: Eligible for ICR, IBR 2009, and RAP (once available)

- IDR Profile 4: Eligible for IBR 2009 only

- IDR Profile 5: Eligible for ICR only

- IDR Profile 6: Eligible for RAP only (coming soon…)

See the WikiDebt IDR Profiles page for more details.

The Repayment Assistance Plan (RAP)

New graduates will also have access to the upcoming RAP option, scheduled to be available by July 1, 2026. Currently, nothing prevents eligible borrowers from switching between legacy income-driven plans and the new RAP option.

Being able to use the new RAP option alongside the legacy plans provides the most repayment flexibility and the lowest total repayment cost opportunity. RAP is going to be the preferred repayment option to start with for nearly all new graduates, once it becomes available. New graduates should plan to apply for RAP using their 2025 federal income tax return about 60 days before their Direct Loan grace period ends.

Use the VIN Foundation Student Loan Repayment Simulator to see how the new RAP option compares to the Standard and IBR options.

Health Professions Student Loans (and other non-Direct federal loans)

Usually, we encourage new graduates with Health Professions Student Loans (HPSL), Loans for Disadvantaged Students (LDS), or Perkins Loans to consolidate those non-Direct Loans into a Direct Consolidation Loan. Doing so allows you to repay more of your balance using federal income-driven repayment plans, and also makes those non-Direct Loan balances eligible for Public Service Loan Forgiveness (PSLF).

Unfortunately, consolidating this year will most likely result in the loss of the legacy income-driven options for your entire federal student loan balance since you’re unlikely to receive that Direct Consolidation Loan before July 1st. Please do not consolidate your non-Direct Loans. Instead, repay them separately using their required standard 10-year plan after their post-graduation grace period expires (12-month for HPSL and LDS, 9 months for Perkins Loans).

If you are pursuing an internship and/or residency, HPSL and LDS can be deferred interest-free for the duration of your training.

2026 Consolidation Exception

Consolidation Exception: If you are graduating in 2026 and starting a new academic program (like a PhD program) before your veterinary school student loan grace period expires, you may want to consolidate your loans before you start that program and get your loans into the new RAP option. These are rare but consequential student loan repayment scenarios. The higher your student loan balance and the longer your post-graduate program, the more likely it is that consolidating will help you: 1) end your grace period and get your loans into a forgiveness-eligible repayment plan, 2) prevent interest from accruing for the duration of your post-graduation program using the new RAP option. You will, however, lose access to the legacy income-driven plans by doing so.

To learn more about specific repayment strategies for the class of 2026, participate in the Debt Repayment Prep Challenge and join the New Grad Student Loan Repayment Playbook webinar on April 22, 2026.

2026 New Grad Student Loan Repayment Playbook

To learn more about specific repayment strategies for the class of 2026, review the New Grad Student Loan Repayment Playbook webinar recording.

Need student loan help?

Have more questions? Post a comment below or email [email protected].

We’re here to help!

Dr. Tony Bartels graduated in 2012 from the Colorado State University combined MBA/DVM program and is an employee of the Veterinary Information Network (VIN) and a VIN Foundation Board member. He and his wife have more than $400,000 in veterinary-school debt that they manage using federal income-driven repayment plans. By necessity (and now obsession), his professional activities include researching and speaking on veterinary-student debt, providing guidance to colleagues on loan-repayment strategies and contributing to VIN Foundation initiatives.