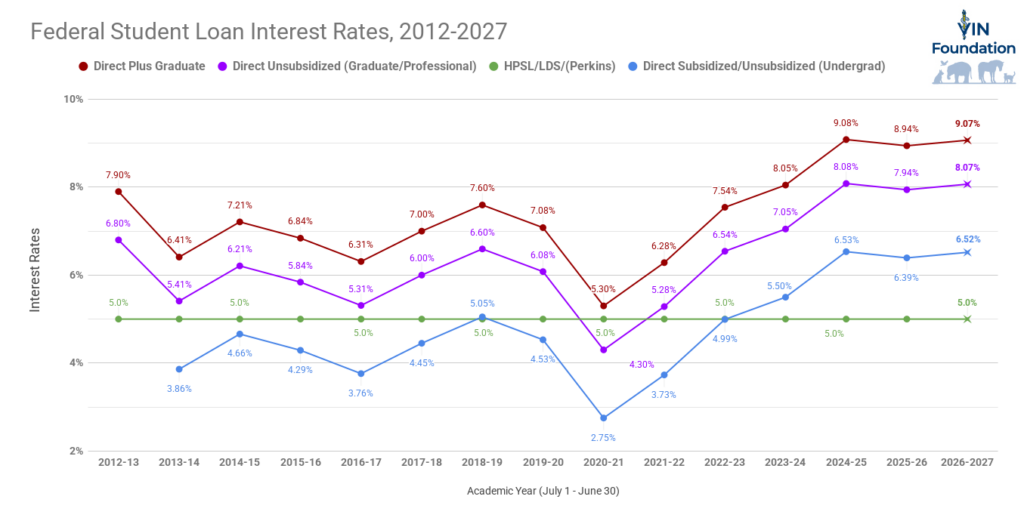

Student Loan Interest Rates Rise for 2026-2027 Academic Year

Federal Direct Loan interest rates for graduate school break their upward trend Federal student loan interest rates have a fixed rate for the life of the loan. That fixed interest rate depends on when you receive the loans. Each spring, we closely monitor the federal treasury yields. With all of the economic uncertainty this year, […]

Student Loan Interest Rates Rise for 2026-2027 Academic Year Read More »